Life update: I changed how I’m working, and got a job working for someone else again!

I’ve been 100% freelance consulting for the last 2.5 years, and in the last year or so, I started to realize:

1 / that I might actually be recovered from the burnout of working fulltime in NYC during peak pandemic then moving across the country,

2 / that something was missing: colleagues!

3 / That I wanted to learn more and do the specific experiments you can run when you’re doing the work, not coaching the work. I am a practitioner at heart.

4 / That I wanted to have bigger impact – and tie together the innovation, strategy, business design, horizontal/democratic workplace, and UXR/product work I do

HOW I GOT THIS NEW JOB

So after I finished Have a Nice Life, I took a lap around the organizations and people I know: I let folks know I was looking. I looked specifically into jobs that would let me have a leadership position, and that worked in ways which align to how I want to be in the world: collaborative, democratic, and making things that make a difference.

Ultimately, I applied for 12 jobs [a few of these more as warm-up than jobs I truly wanted], three of which I had referrals in to. I interviewed for two interesting jobs [notably: both of these were from a referral or a personal connection]. I got an offer in June, and started the new role in early July after I wrapped up some client projects and took a week off!

I negotiated a 4-day week, having specifically selected a potential employer who I knew offered this option — which means I still have a day a week for client projects, coaching, and workshops here at Ride Free. I love doing this work! I just never want to do it [or anything] alllllll the time. #geminiproblems. I also negotiated more PTO than they originally offered: friends, always negotiate!

HOW I BUDGETED AROUND MY NEW JOB

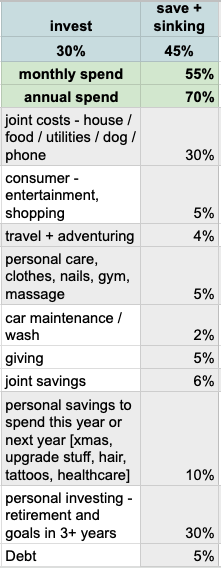

An additional feature of this decision is I’ll be making more money – so, I reviewed what’s true about my costs, goals, and income today. Here’s how I decided to split it:

> 35% needs

- 30% – pays my share of the mortgage, food, doggo care, utilities – I pay 65% and my partner pays 35%, adjusted for our different incomes.

- 5% – debt: I got a 0% loan to solve an expensive problem in my house so I’m paying it off over 10 months before interest comes due – this felt safe to do because I could pay it off if needed, but wanted to hold off in case the house problem was somehow even more expensive to fix [turns out, it was].

> 15% wants [eg discretionary/fun money]

- discretionary and fun money: gym, clothes, entertainment, travel, personal care, consumer stuff, thrifting, car maintenance for my old paid-off Subaru

> 50% goals, gifts, savings

- 5% – giving! ½ to my mom and ½ to organizations and other people I care about

- 16% – savings for stuff in the next year or two: for house maintenance and upgrades, my doggo, holidays, haircuts, tattoos, stuff upgrades/maybe a new car eventually, etc. This meant reviewing my semi-annual savings plans and adjusting some of the amounts I put aside each month.

- 29% – long term investing – retirement and investing for things I want when I’m 50 [shockingly, in 5 short years]. This feels low to me but I’ll absorb the money from my debt payment into this, after the loan is cleared.

I had to set up new accounts with the job and made sure the right people were beneficiaries on my retirement accounts – because these supersede your Will, and I want to make sure the people I think will need my money if I leave this plane early, get it. Finally, after my first paycheck came through, I adjusted all my automated savings and investments to match my new plan and the times in the month when I get paid.

Now, to recover from starting a new job and needing every brain cell to learn allllll the new things.